Understanding California’s Proposition 19

By Kurt Real Estate Mar 8, 2021

California Proposition 19 is known as “The Home Protection for Seniors, Severely Disabled, Families, and Victims of Wildfire or Natural Disasters Act.”To assist taxpayers, the following provides general information on Proposition 19. Please continue to visit the California State Board of Equalization (BOE) website for updates, as additional legislation will provide further clarification. For assistance or questions, please contact the Property Tax Department by phone at 1-916-274-3350 or by e-mail.

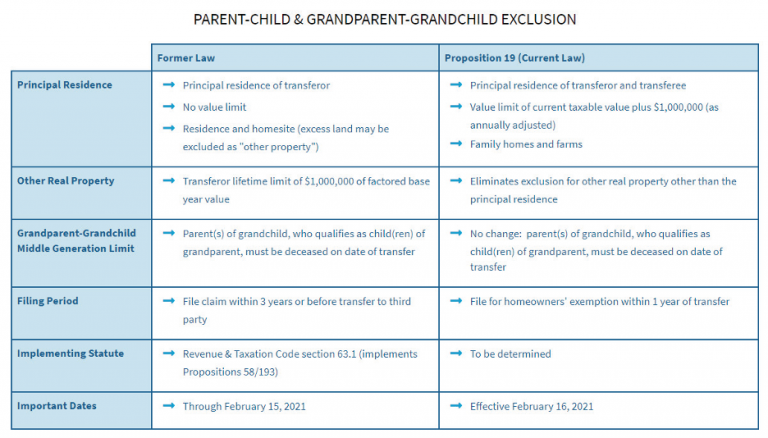

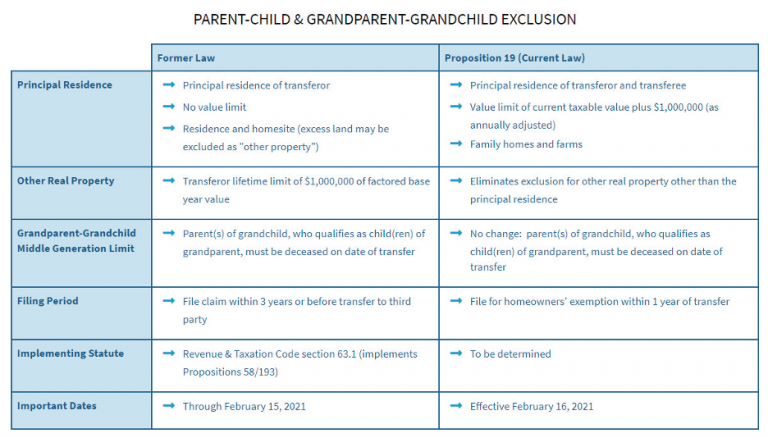

Below are comparison charts reflecting the effects of Proposition 19

What is the effective date of Proposition 19?

Proposition 19, which was passed by the California voters on November 3, 2020, became effective on December 16, 2020, the 5th day after the Secretary of State certified the election. However, the changes to the parent-child and grandparent-grandchild exclusion will become operative and apply to transactions on February 16, 2021, and the base year value transfer provisions will become operative on April 1, 2021. Does the Board of Equalization have the authority to extend or change Proposition 19’s operative dates of February 16, 2021 or April 1, 2021? No. The Board of Equalization does not have the authority to extend or change Proposition 19’s operative dates of February 16, 2021 or April 1, 2021.

Base Year Value Transfers

Under Proposition 19, will I qualify for the base year value transfer if I purchase my replacement home now and sell my original home on or after April 1, 2021? Proposition 19 requires the transfer of the base year value to occur on or after April 1, 2021. It does not require that both the primary residence be sold and the replacement primary residence be purchased on or after April 1, 2021. Therefore, in most cases, as long as either the primary residence is sold or the replacement primary residence is purchased on or after April 1, 2021, the base year value of the primary residence can be transferred to the replacement primary residence under Proposition 19. However, future legislation may impact the operation of Proposition 19 and any updates will be posted on the Board’s website. For More Information Visit: https://www.boe.ca.gov/prop19/#Guidance

Under Proposition 19, will I qualify for the base year value transfer if I sell my original home now and purchase a replacement home on or after April 1, 2021?

As answered in the prior question, as long as either the primary residence is sold or the replacement primary residence is purchased on or after April 1, 2021, the base year value of the primary residence can be transferred to the replacement primary residence under Proposition 19. For example, a person over age 55 years old who has already sold their original home and expects to purchase a replacement home on or after April 1, 2021, would qualify for Proposition 19 base year transfer.

Is Proposition 19 retroactive and would it cause property transfers that have already received the benefit of Proposition 60/90 to be reassessed?

The Proposition 19 operative date for the base year value transfer provisions is April 1, 2021. It is not expected that base year value transfers that have already been processed under Propositions 60/90 and Proposition 110 will be affected.

If I use my one-time base year value transfer under Proposition 60/90, can I transfer that base year value three more times under Proposition 19?

It is anticipated that three transfers under Proposition 19 will be allowed regardless of whether a property owner transferred a base year value in the past under Propositions 60/90 and Proposition 110. Future legislation may impact the operation of Proposition 19 and any updates will be posted on the Board’s website.

Under Proposition 19, can I transfer my base year value to a home of any value?

Yes; however, if the full cash value of the replacement home is greater than the full cash value of the original home, the difference in full cash values will be added to the transferred factored base year value.

For example, an original home was sold and had a full cash value of $400,000 and a factored base year value of $100,000 at the time of sale. If a replacement home is purchased for a full cash value of $600,000, the difference of $200,000 ($600,000 – $400,000) is added to the factored base year value of $100,000. Thus, the replacement home will have a new base year value of $300,000 ($100,000 + $200,000).

Is Proposition 19 retroactive to disasters that occurred in 2020?

Proposition 19 is effective on and after April 1, 2021, and also requires that a replacement primary residence is purchased or newly constructed as a person’s principal residence within two years of the sale of the original primary residence. Proposition 19 is not dependent on the date of disaster. However, future legislation may impact the operation of Proposition 19 and any updates will be posted on the Board’s website.

To qualify for the base year value transfer, does the homeowner have to be (1) age 55 or over and (2) disabled, and (3) a victim of a disaster (all three)? No, under Proposition 19, a homeowner may qualify for the base year value transfer under any one of the three categories listed; they do not need to meet all three categories in order to qualify.

Parent-Child and Grandparent-Grandchild Transfers

Is Proposition 19 retroactive and would it cause property transfers that have already received the benefit of Proposition 58 (Parent-Child Exclusion) to be reassessed?

No, Proposition 19 is clear that Proposition 58 applies to transfers that occur on or before February 15, 2021, and that Proposition 19 applies to transfers that occur on or after February 16, 2021.

If a family home is gifted to two children, do both children have to reside in the family home as their primary residence in order to receive the parent-child exclusion?

We believe the intent of the Legislature was to allow the exclusion as long as the parent’s family home becomes the family home of at least one of the children.

Under Proposition 19, if I inherit my parent’s family home and move into it and establish it as my principal residence, must I live continually in the home to receive the parent-child exclusion? What happens if I move somewhere else?

We believe that at least one eligible transferee must continually live in the property as his or her family home for the property to maintain the exclusion. Thus if the property is no longer your family home, it will receive a new taxable value. The new taxable value will be the fair market value of the home on the date you inherited it, adjusted each year for the inflation factor, which is published by the BOE annually.

See https://www.boe.ca.gov/proptaxes/countycontacts.htm

Does Proposition 19 apply to a transfer of a rental home?

No, Proposition 19 limits the parent-child exclusion to a transfer of a family home that is the principal residence of the transferor and becomes the principal residence of the transferee.

Do we need to submit our application for the parent/child exclusion prior to the February 16, 2021 operative date to qualify for the exclusion under Proposition 58/193?

As long as the date of transfer or change in ownership of real property between parent and child occurs on or before February 15, 2021, the transfer will qualify for the exclusion under Proposition 58/193. Therefore, as long as the claim is filed with the County Assessor within three years of the date of transfer or before a transfer to a third party or within six months of the date of notice of supplemental or escape assessment. Thus, the claim does not need to be filed by February 16, 2021.

Will I lose the parent-child exclusion if the value of the family home is greater than $1 million dollars?

The value limit under Proposition 19 is the sum of the factored base year value plus $1 million. If the market value exceeds this limit, partial relief is available. The amount exceeding the excluded amount will be added to the factored base year value.

For example, a family home has a factored base year value (FBYV) of $300,000 and a fair market value of $1,500,000. The excluded amount under Proposition 19 is $300,000 + $1,000,000 = $1,300,000. The difference, $1,500,000 – $1,300,000 = $200,000. Thus, the adjusted base year value is $500,000 (FBYV $300,000 + difference of $200,000).

If a parent died prior to the February 16, 2021 operative date and the Assessor does not become aware of the death until a year later and reassesses the property as of the date of death, are the parent-child exclusion provisions applied under Proposition 58 or Proposition 19?

The date of death is the date of the change in ownership. The law in effect as of the date of death will apply. Proposition 19 is clear that Proposition 58 applies to transfers that occur on or before February 15, 2021, and Proposition 19 applies to transfers that occur on or after February 16, 2021.

I have my deed signed and notarized, and have submitted it for recording at my local County Recorder’s office prior to the February 15, 2021 deadline. What if my deed does not record by the February 15, 2021 deadline? Must my deed be recorded prior to that date in order to still be under the Proposition 58/193 provisions?

No. As long as the date of transfer is on or before February 15, 2021, the transfer will qualify for Proposition 58/193 exclusion. Property Tax Rule 462.260 makes clear that the recordation date of a deed is rebuttably presumed to be the transfer date. This means that if the evidence is shown that the transfer occurred prior to the recordation date, the assessor should accept that earlier date. Such evidence could be, for example, the date of a notarized document of transfer, such as a deed.

How is a property held in a trust affected by Proposition 19?

The administration of a trust is governed by the trust instrument itself. For properties held in trusts, Revenue and Taxation Code section 61(h) provides that a change in ownership occurs when any interests in real property vest in persons other than the trustor or the trustor’s spouse or registered domestic partner when a revocable trust becomes irrevocable (also see Property Tax Rule 462.260). This typically occurs upon the death of the trustor. Thus, the date of death is considered to be the date of a change in ownership. Proposition 19 is clear that Proposition 58 applies to transfers that occur on or before February 15, 2021, and Proposition 19 applies to transfers that occur on or after February 16, 2021.

How do I apply for the homeowners’ exemption or disabled veterans’ exemption within one year of the transfer to qualify for the parent-child or grandparent-grandchild exclusion, as required by Proposition 19?

To apply for the homeowners’ exemption or disabled veterans’ exemption, a claim must be filed with the County Assessor. BOE-266, Claim for Homeowners’ Property Tax Exemption, is the claim form to apply for the homeowners’ exemption, and BOE-261, Claim for Disabled Veterans’ Property Tax Exemption, is the claim form for the disabled veterans’ exemption. Both forms can be obtained from and submitted to the local County Assessor’s office where the property is located

I still have questions on Proposition 19. Who do I contact to discuss?

If you have further questions, you may call the Board of Equalization’s Property Tax Department, County-Assessed Properties Division at 1-916-274-3350 or by e-mail.

Source: boe.ca.gov/prop19/#charts

This article is a reproduction of the source credited above. Please note that any advice, whether legal or otherwise, is the opinion of the author. The Kurt Real Estate Group Inc. would encourage any person with legal questions relating to this topic to seek an independent legal opinion.

Meet Kurt Galitski

The Kurt Real Estate Group Inc. Call Them Today 877-957-6677

Distinctive Strategies that Deliver Record-Setting Results!

When you combine Kurt’s passion and knowledge of the real estate market, you really gain an appreciation for what makes Kurt different. But what truly sets him apart from the crowd are his 5 distinctive strategies…

For Kurt, getting into real estate was not an accident, it was a deliberate and calculated decision to deliver a better experience to home buyers and sellers than they have ever received before. Today, you could ask any one of hundreds of clients, read his Yelp reviews, or look at his track record of being awarded in Orange Coast and Forbes Magazine in excess of ten consecutive years and you too will say mission accomplished.

You can call him direct on his cell at 714-957-6677

Kurt Galitski | The Kurt Real Estate Group | Top 2% Coldwell Banker Agents Nationally | BRE# 01348644 | www.KurtRealEstate.com https://youtu.be/9c0h4KCgKUQ Kurt@KurtRealEstate.com

All Articles

Recent Post

Join our network

Keep up to date with the latest market trends and opportunities in Orange County.